If you are covered by a pension at work, you are considered “covered by a retirement plan” under IRS rules. That does not mean you cannot contribute to a Traditional IRA.

It means your ability to deduct that contribution depends on income.

This is where many nurses get tripped up, so let’s slow it down and look at the actual 2026 rules.

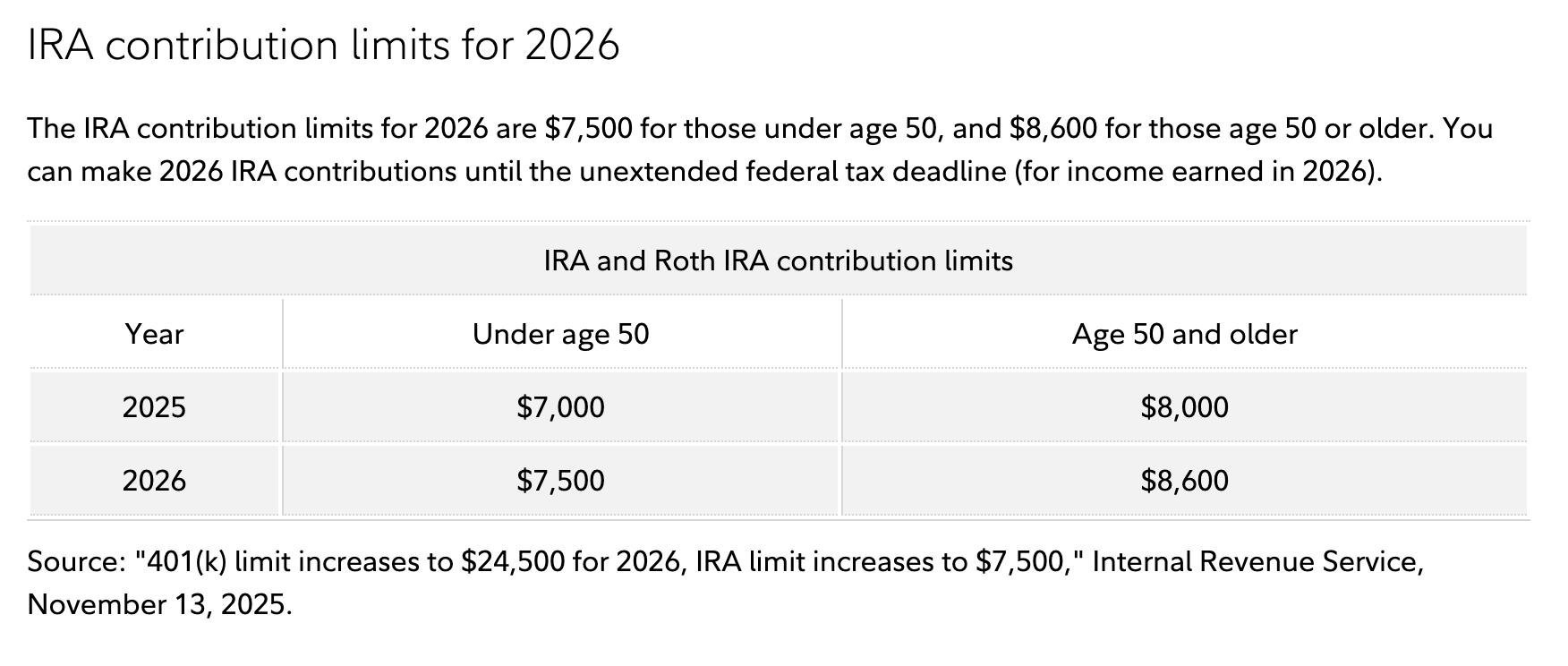

Step 1: Contribution Eligibility

If you have earned income, you can contribute to a Traditional IRA.

For 2026, the contribution limit is $7,500 (plus catch-up if eligible).

Your pension does not block contribution.

Now let’s talk about deductibility.

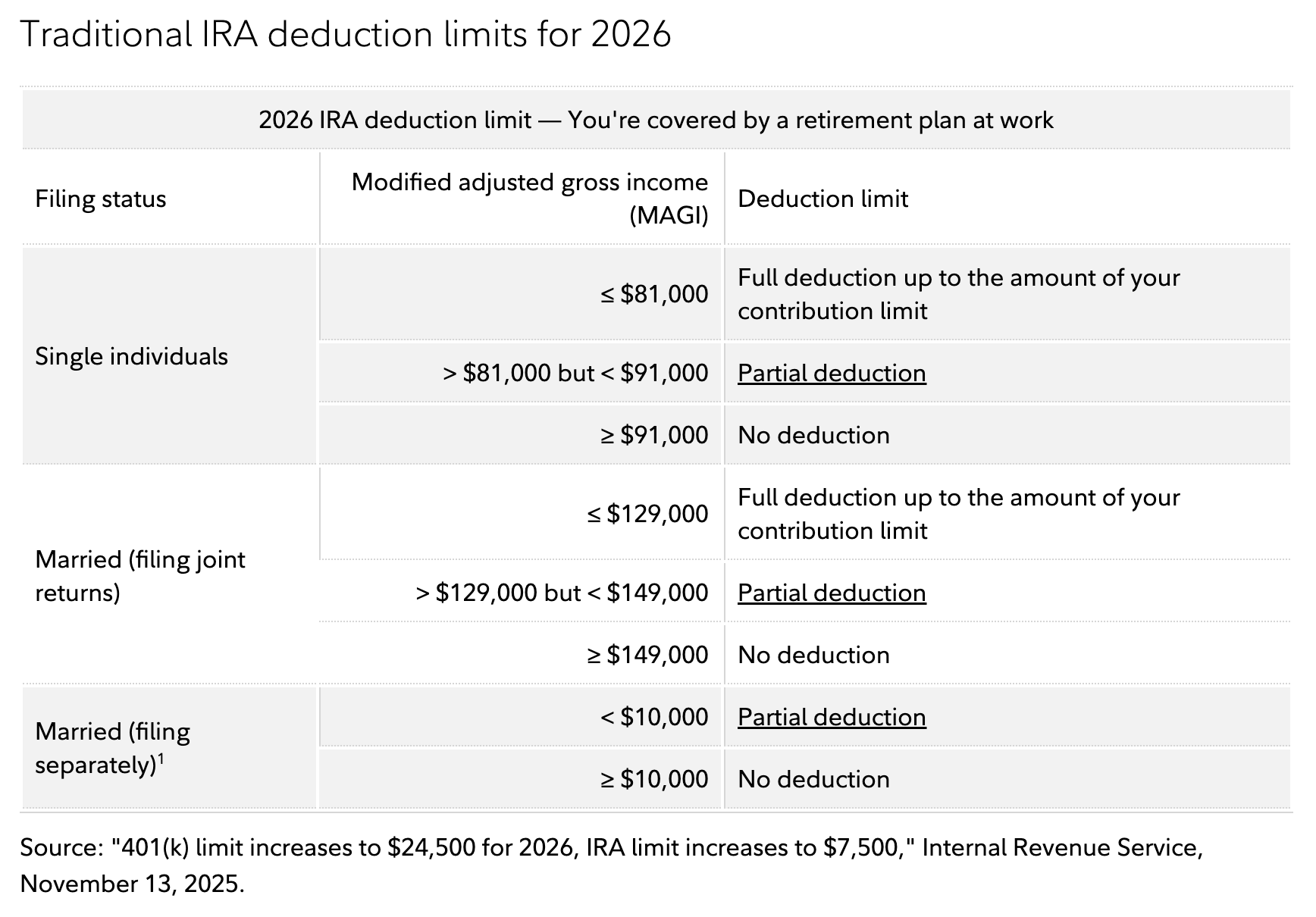

If You Are Covered by a Retirement Plan at Work (Your Pension Counts)

If you are covered by a plan at work, your ability to deduct your Traditional IRA contribution depends on your Modified Adjusted Gross Income (MAGI).

Here are the 2026 deduction limits:

What this means in real life:

If you are single and earn $75,000 → Full deduction.

If you earn $85,000 → Partial deduction.

If you earn $95,000 → No deduction.

You can still contribute. You just may not get the upfront tax break.

For married nurses filing jointly, notice how the phaseout range is higher.

That’s why filing status matters in retirement planning conversations.

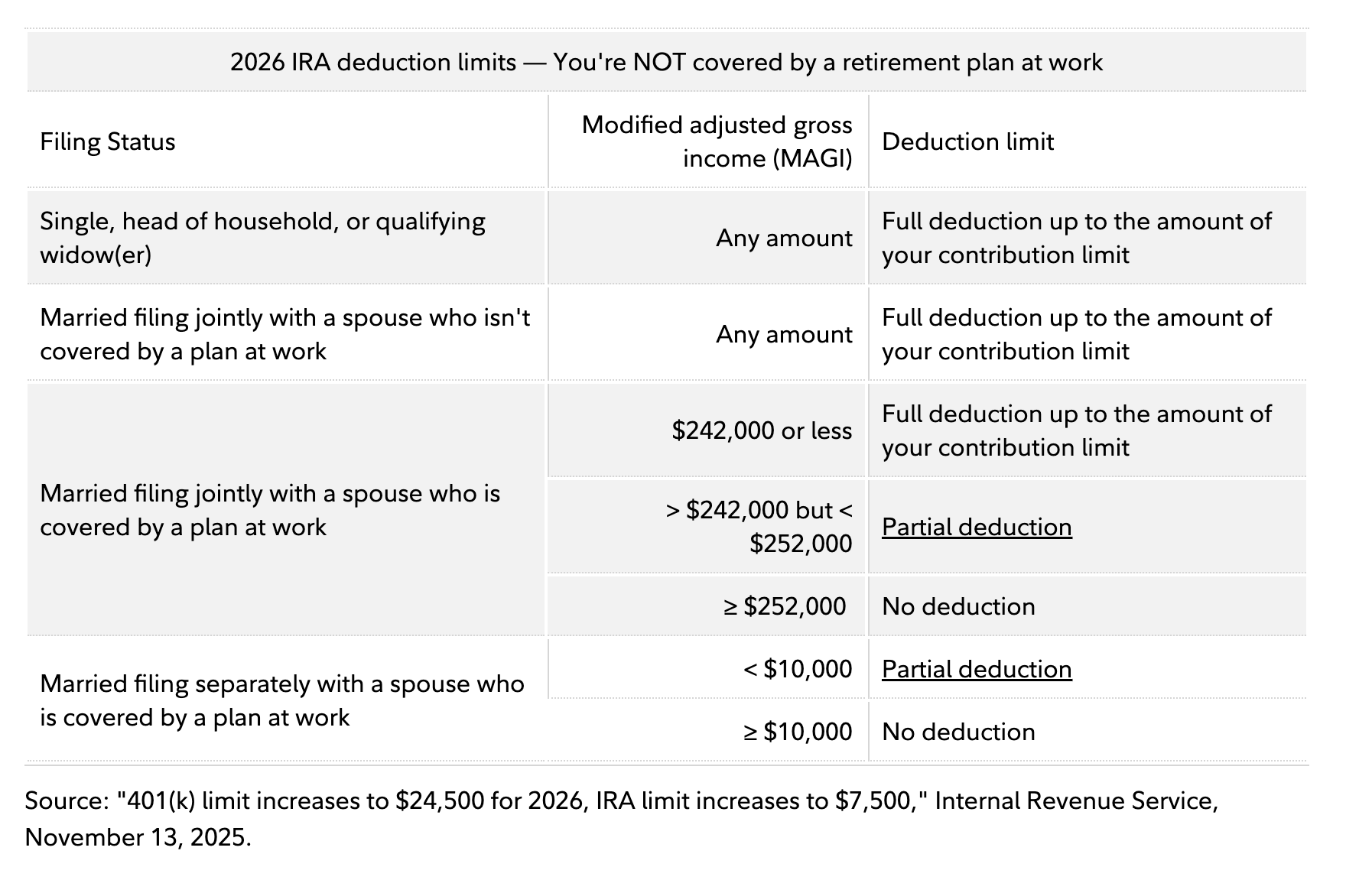

If You Are NOT Covered by a Retirement Plan at Work

This section applies less often to our community because most hospital nurses with pensions are considered covered.

But it matters in dual-income households.

For example:

-

You are a nurse with a pension.

-

Your spouse is not covered by a retirement plan.

In that case, different income thresholds apply.

Here are the 2026 rules if you are NOT covered:

The nuance here is important.

If you personally are not covered by a plan at work, you may qualify for a full deduction regardless of income: unless your spouse is covered and your household income exceeds certain thresholds.

This is where spousal IRA planning becomes powerful.

The Strategic Layer for Pension Nurses

Now let’s zoom out.

When you have a pension, you are building future taxable income in retirement.

Your pension payments will generally be taxed as ordinary income.

So when deciding between:

-

Traditional IRA (pre-tax today, taxed later)

-

Roth IRA (taxed today, tax-free later)

-

Non-deductible Traditional IRA

-

Backdoor Roth

We are not just asking, “Can you deduct it?”

We are asking:

What does your future tax picture look like?

If your pension is projected to replace a large percentage of your income, adding more pre-tax dollars may not always be optimal.

If your income is too high to deduct, a Roth strategy may be cleaner.

If you are in the phaseout range, partial deductions require precision and proper tracking via Form 8606.This is not about memorizing IRS charts.

It’s about understanding the difference between:

Contribution eligibility and

Deductibility.

Those are separate rules.

And when you understand them, you stop leaving retirement tools unused because of misinformation.