Let’s break down the strategies and the stories behind them.

You’ve probably heard that making extra mortgage payments can save you “a lot” over time…

But how much is “a lot”? And what does that really look like in real life?

Let’s zoom in on an example from someone we’ll call Stephanie.

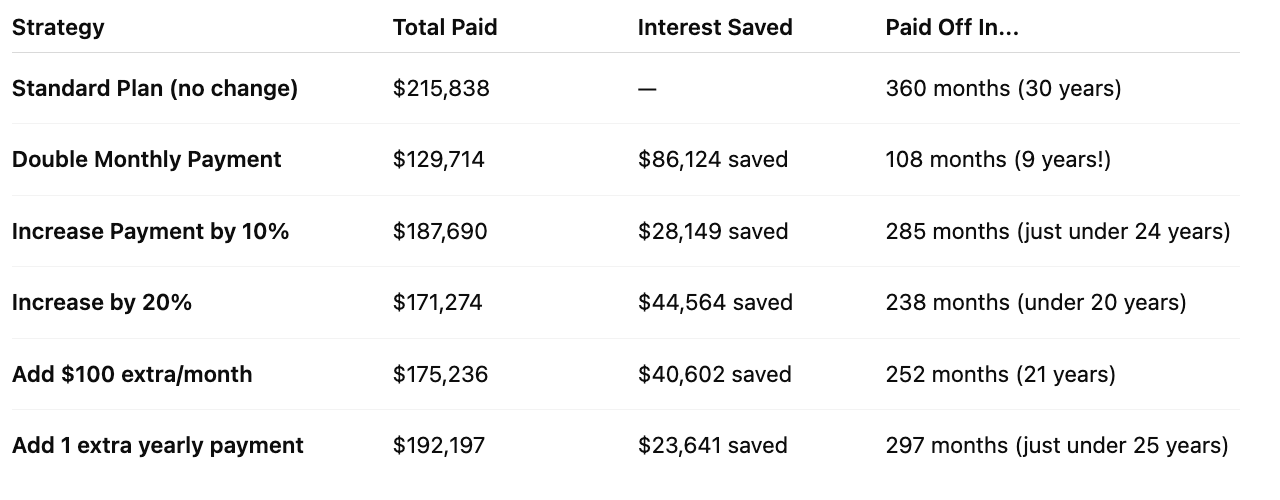

She has a $100,000 mortgage at 6%, with a monthly payment of $599.55.

If she pays it off as scheduled (30 years), she’ll pay a total of $215,838.

That includes $115,838 in interest.

Now let’s see what happens when she makes small but consistent shifts to her payment rhythm:

5 Ways to Pay Off a Mortgage Faster and What It Saves:

So... what does this mean for you?

Big takeaway?

You don’t need to double your payment to make a big impact.

Just adding $100/month could save you over $40,000 in interest and cut your loan by 8 years.

🧠 Strategy vs. Emotion: Why We Really Want to Pay Off Early

Let’s be honest.

Most people aren’t doing this just to save money.

You might be thinking:

“I just want it gone.”

“I hate seeing that debt.”

“I want to feel safe.”

That’s emotional.

And it’s valid.

But your financial plan has to hold both the math and the mental load.

NurseMoneyDate® Check-In:

Before you start throwing extra money at your mortgage, ask:

-

Do I have a fully funded emergency fund?

-

Am I still investing in retirement or other long-term goals?

-

Am I choosing this from clarity or from fear or pressure?

-

Would paying extra still leave room for joy, margin, and rest?

There’s nothing wrong with wanting to be mortgage-free.

But we don’t use debt payoff as a replacement for emotional safety.

We build that first—with structure, not stress.

Final Thought:

If it brings peace, round up your payment.

If it adds pressure, pause.

This isn’t about impressing anyone.

It’s about designing a life where you feel rooted, not restricted.