What That Confusing 1099-R Is Actually Telling You

One of the things I’m learning deeper in my CFP® journey is this:

tax forms don’t explain themselves and they often look scarier than they are. A perfect example? The Form 1099-R you receive after doing a backdoor Roth conversion.

I recently saw a great breakdown from one of my CFP® mentors, and it highlights a mistake I see all the time: people accidentally paying tax twice on the same money because they misunderstand what the form is saying.

Let’s slow this down.

Why Your 1099-R Looks “Wrong” (But Isn’t)

If you completed a backdoor Roth conversion, you’ll receive Form 1099-R showing the money that left your Traditional IRA.

Here’s what usually causes panic:

-

Box 1 (Gross distribution) shows the full amount moved

-

Box 2a (Taxable amount) often shows that same full amount

-

Box 2b is checked: “Taxable amount not determined”

Cue the stress spiral.

“Wait… I thought backdoor Roths were non-taxable?? Why does this look fully taxable?”

This is where context matters.

The Custodian Doesn’t Know Your Tax Story

Your IRA custodian: whether it’s Fidelity, Vanguard, or another firm does not know whether your Traditional IRA contributions were:

-

Deductible (pre-tax)

-

Non-deductible (after-tax)

-

Or a mix of both

So they default to:

👉 “Here’s the distribution. You figure out the taxes.”

That’s why Box 2b matters more than people realize.

The Form That Actually Prevents Double Taxation

The real hero here is Form 8606.

This is where you report:

-

Your non-deductible Traditional IRA contributions

-

Your IRA basis (after-tax money)

-

How much of the Roth conversion is actually taxable

That information usually comes from Form 5498, which shows your contributions.

Once Form 8606 is completed correctly, the IRS can see:

-

What portion was already taxed

-

What portion (if any) is taxable now

This is how you avoid paying tax twice on the same dollars.

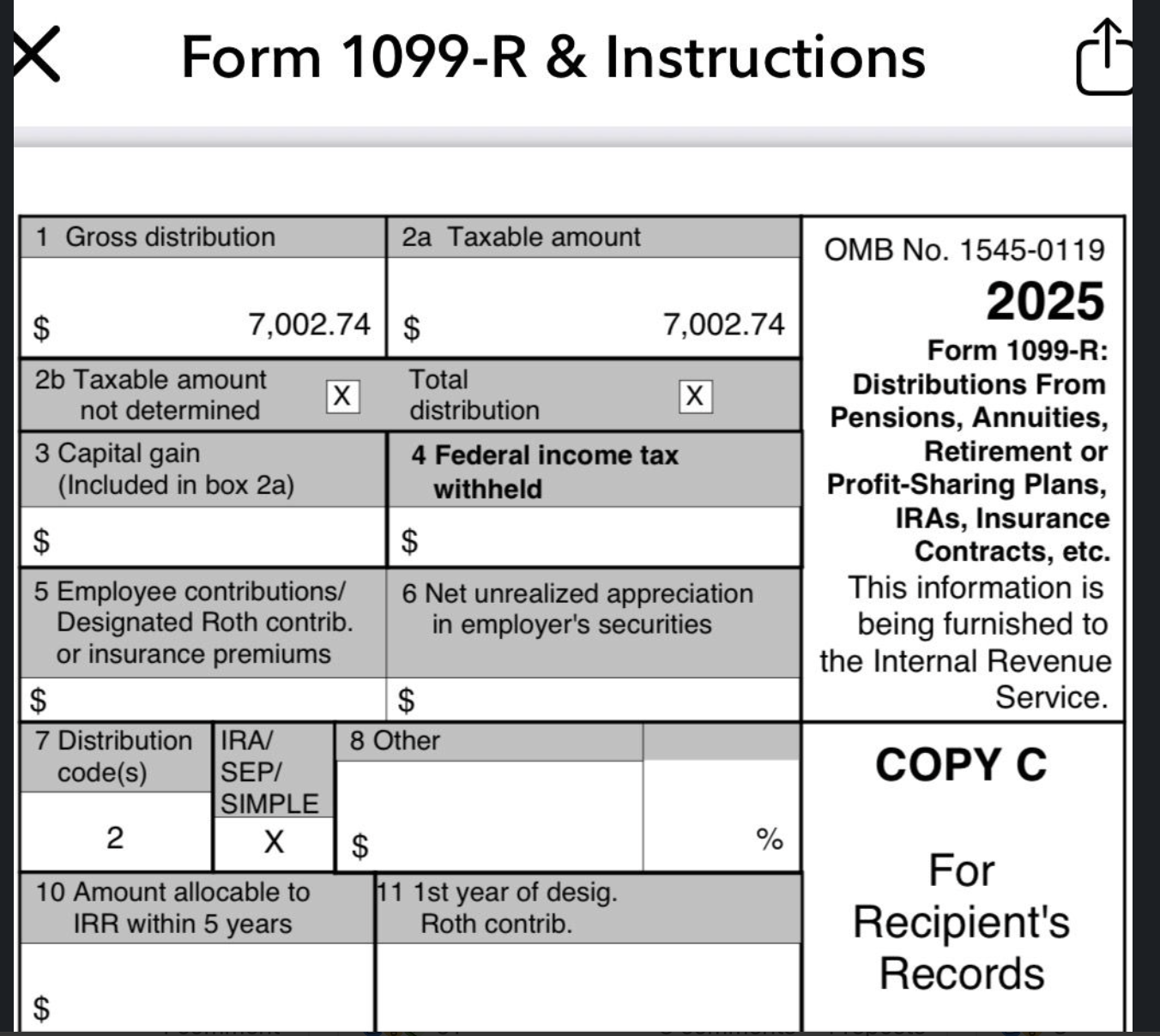

A Simple Example

Let’s make this concrete:

-

You contribute $7,000 to a Traditional IRA (non-deductible)

-

Before converting, it earns $2.74

-

You convert $7,002.74 to a Roth IRA

Your 1099-R will likely show:

-

$7,002.74 as the gross distribution

-

$7,002.74 in Box 2a

But after Form 8606:

-

$7,000 is non-taxable (already taxed)

-

$2.74 is taxable (the growth)

That’s it.

The form looked dramatic the tax impact was minimal.

The Bigger Lesson (And Why I’m Sharing This)

This is one of those moments where financial confidence isn’t about knowing more, it’s about knowing where to look.

The mistake isn’t doing a backdoor Roth.

The mistake is assuming the IRS or your brokerage will automatically connect the dots for you.

They won’t.

And that’s why learning how these pieces fit together: 1099-R, 5498, 8606 is such an important part of building long-term wealth without unnecessary stress or overpayment.

Bottom Line

-

A “taxable” amount on your 1099-R does not automatically mean you owe tax

-

Backdoor Roths require proper reporting, not blind trust

-

The goal isn’t perfection it’s not paying more than you owe

This is exactly the kind of nuance I’m learning (and unlearning) as I go deeper into my CFP® work and it’s why I care so much about helping nurses feel calm and capable around money decisions like this.